Social Security is the largest single program in the federal budget, costing $1.6 trillion in fiscal year 2025—about 22% of total federal spending. Because of its scale, Social Security plays a major role in shaping the nation’s fiscal outlook. However, its unique trust fund structure makes it harder to understand how the program contributes to deficits and debt over time. This post breaks down how Social Security is financed and why it’s adding pressure to the federal budget.

What Are the Social Security Trust Funds?

Social Security is funded through two separate accounts:

- Old-Age and Survivors Insurance (OASI)

- Disability Insurance (DI)

Together, they’re often referred to as the Social Security trust fund. Payroll taxes and other dedicated revenues flow into these funds, which are then used to pay benefits and administrative costs.

As of August 2025:

- The OASI fund supports 61.96 million beneficiaries and is much larger than the DI fund.

- The DI fund serves 8.32 million people and is financially stable, projected to remain solvent for at least 75 years.

- The OASI fund, however, is projected to run out of reserves by 2032. Without reform, that would trigger a 24% cut in benefits.

How the Social Security Trust Fund Works

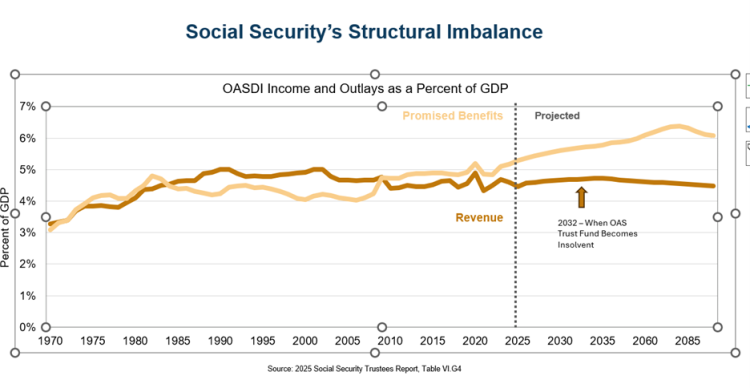

Social Security is mostly a “pay-as-you-go” system: payroll taxes from today’s workers are used to pay benefits to today’s retirees and other recipients. From 1984 through 2009, the program collected more in revenue than it spent. These surpluses didn’t sit in a savings account—they were used to buy special Treasury bonds. The federal government spent the proceeds from these bonds on other programs, but it’s legally obligated to repay those bonds with interest when Social Security needs the funds to cover benefits.

Since 2010, Social Security has run annual cash-flow deficits—bringing in less revenue than it spends. To make up the difference, the program has tapped into its “trust fund reserves” to pay out full benefits. These reserves only exist on paper and serve primarily as a way to track how much of the historical Social Security surpluses the federal government has spent. In reality, the surplus has not been saved, instead the Treasury has borrowed roughly $1.08 trillion from 2010 to 2023 to meet Social Security’s obligations.

How Social Security Will Continue to Put Pressure on the Federal Deficit

Looking ahead, Social Security’s financial shortfall is expected to grow. According to the latest Trustees report, covering these annual deficits—from 2025 to 2032— will require more than $2.5 trillion from the Treasury by 2032. According to estimates from the Committee for a Responsible Federal Budget (CRFB), over that same period, coverage for the total annual deficits will require $16.7 trillion. So about 15% of that total is directly tied to keeping Social Security benefits fully funded under current law.

In 2032, the Social Security trust fund will run out of reserves. As noted above, these reserves were never cash in a vault—they were essentially IOUs from the U.S. Treasury to the Social Security system. Once those IOUs are exhausted, the government will no longer have the legal authority to borrow additional funds to pay full OASI benefits and benefits will have to be cut to match revenues collected. What this means is that without legislative action, all beneficiaries could see an estimated 24% cut in payments, regardless of income or need.

Conclusion

In short, while Social Security is often viewed as a self-financing program, its growing mismatch between dedicated revenues and benefit obligations is placing increasing strain on the federal budget. The trust fund’s past surpluses have already been spent, and the government must now borrow over $2 trillion to redeem those IOUs and cover benefit payments through 2032. At that point, Social Security will no longer have borrowing authority and policymakers will face a choice about how to sustainability finance the program into the future.. Addressing this structural imbalance is not just about preserving benefits for future retirees; it’s also essential to restoring long-term fiscal sustainability.

Continue Reading