Many people think of Social Security as a system where you simply get back roughly the amount of money you put in during your working years. But Social Security was never designed that way. Instead, it operates primarily as a pay-as-you-go system — meaning that today’s workers pay taxes that fund the benefits of today’s retirees. The money you pay into Social Security isn’t sitting in an individual account waiting for you; it’s immediately used to support current beneficiaries. In fact, the amount you receive in benefits is based on a progressive formula that replaces a larger share of income for workers with lower lifetime earnings.

How Does Social Security Really Work?

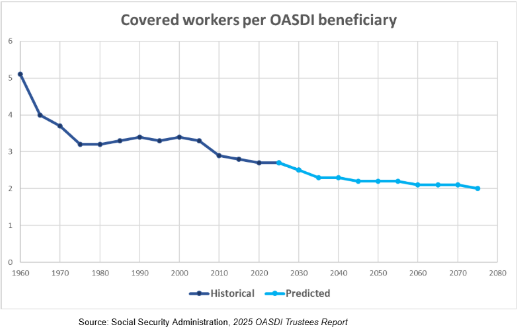

Social Security is built on a foundation of intergenerational support. Each generation pays into the system to help the generation before them, and in turn, the next generation will do the same for them. This structure means that the system’s sustainability depends on the balance between workers and retirees and the overall health of the economy. Unfortunately the system is currently out of balance because the ratio of workers to retirees has declined due to the Baby Boom generation’s retirement combined with rising life expectancy and declining fertility rates. In 1960, the ratio of payroll taxpayers to Social Security beneficiaries was five to one. Today, there are fewer than three workers for every beneficiary. And by 2030, the ratio of payroll taxpayers to Social Security beneficiaries will drop to 2.5 to one.

The disconnect between taxes paid and benefits received is also impacted by Social Security’s progressive benefit structure. What does this mean? Simply put, people with lower lifetime earnings receive a higher proportion of their pre-retirement income in benefits compared to those with higher earnings. This design helps provide a social safety net for lower-income workers and reduces poverty among the elderly.

Demonstrating the Relationship Between Taxes Paid and Benefits Received

To help illustrate this, here’s a simplified table showing the expected present value of lifetime Social Security and Medicare benefits and taxes for hypothetical single workers with different earnings levels retiring in 2025 at age 65. These numbers are in 2025 dollars, discounted to present value at age 65, and assume scheduled benefits are paid even after trust fund depletion.

| Earnings Level | Lifetime Social Security Taxes Paid | Lifetime Social Security Benefits Received | Ratio: Benefits / Taxes |

| Low Earnings (~$35,000) | $185,000 | $251,000 | 1.36 |

| Average Earnings (~$72,300) | $412,000 | $414,000 | 1 |

| High Earnings (~$115,700) | $659,000 | $547,000 | 0.83 |

| Maximum Taxable Earnings (~$176,100) | $1,002,000 | $666,000 | 0.66 |

Source: Urban Institute calculations based on 2025 data.

What Does This Table Tell Us?

- Lower earners receive more in benefits relative to what they pay in taxes. For example, a low earner paying $185,000 in lifetime taxes expects to receive about $251,000 in Social Security benefits—a 36% higher return relative to taxes paid.

- Average earners roughly “break even” on a lifetime basis when looking strictly at Social Security taxes vs. benefits.

- Higher earners receive less in benefits relative to their taxes paid. Those with maximum taxable earnings pay over $1 million in Social Security taxes but receive less than $700,000 in benefits.

This progressive structure reflects Social Security’s goal of providing a stronger safety net for lower-income workers and their families.

Final Thoughts

Social Security is a social insurance program designed to provide economic security, not simply a savings account or investment fund. Its pay-as-you-go nature and progressive benefit formula ensure that it supports those most in need while providing a measure of income replacement for workers as they retire. Understanding this helps us appreciate the system’s purpose and the challenges policymakers face in maintaining its solvency for future generations.

Continue Reading