As Social Security marks its 90th anniversary, a transformative decision about its basic character and financing is being made in silence without deliberation by elected officials or the American people. That decision is whether the program should remain self-financed – with expenditures limited to dedicated income plus past surpluses and interest – or become dependent on general revenue transfers for a significant share of benefit payments.

Each year, the Social Security Trustees deliver a clear message: the program is facing a serious financial shortfall. According to the 2025 Trustees Report, the combined trust funds (Old Age and Survivors Insurance and Disability Insurance, OASDI) will be depleted by 2034. (Note that the Old Age and Survivors Insurance trust fund will be depleted earlier, by 2032.) Once that happens, incoming revenues will only be enough to cover 81 percent of scheduled benefits. In short, an across-the-board benefit cut of nearly 20 percent is less than 10 years away.

Despite this looming deadline and its painful consequences for beneficiaries, Congress has taken no action to shore up the trust funds. Perhaps with two-year election cycles, 2034 still seems far away to members of Congress who imagine that they can act at the last minute – as they do when a government shutdown is pending or when the debt limit must be raised to avoid a default. But waiting to act until the trust funds are on the brink of insolvency has serious consequences, especially for younger generations, and threatens the foundational structure of Social Security itself.

As the Trustees explained in this year’s report, “If substantial actions are deferred for several years, the changes necessary to maintain solvency for the combined OASI and DI Trust Funds would be concentrated on fewer years and fewer generations. Significantly larger changes would be necessary if action is deferred until the combined trust fund reserves become depleted in 2034.”

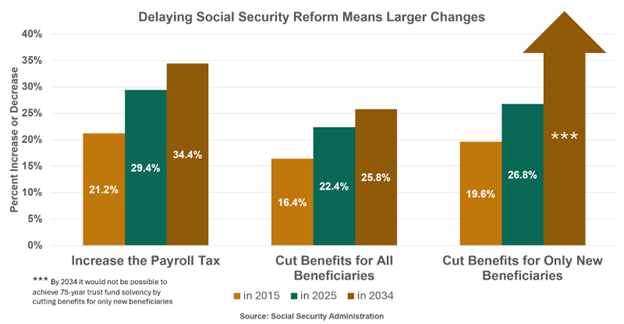

The Trustees lay out a few scenarios to illustrate the point. For example, if Congress wanted to keep the combined OASI and DI Trust Funds solvent for the next 75 years (the standard projection period), they would have to immediately raise the payroll tax by 29 percent or cut scheduled benefits across the board by 22 percent. If they wanted to exempt current beneficiaries, the cut would be 27 percent. They could also use some combination of these approaches but they would have to act this year or the choices become increasingly difficult.

If action is delayed until the trust funds become depleted in 2034, maintaining 75-year solvency would require an immediate payroll tax increase of 34 percent or a reduction in scheduled benefits of 26 percent. By 2034, it would not be possible to achieve 75-year trust fund solvency even if all new benefit claims were eliminated.

Abrupt tax increases or benefit cuts of this size would be so difficult to enact that Congress would likely look to a tempting alternative – using general revenues to bail out the trust funds. This might solve an immediate political problem by avoiding a payroll tax increase or a big benefit cut, but it would merely sweep the substantive problem under the rug. There would still be a growing gap between Social Security’s benefit payments and its dedicated revenues (the payroll tax and taxation of some benefits). The only difference would be that general revenues would fill the gap no matter how large it became. The entire concept of “solvency” would no longer be an issue because Social Security, like the Medicare Supplemental Medical Insurance (SMI) trust fund, would be permanently solvent thanks to its general revenue subsidies. In short, a crisis-induced infusion of general revenues to “save” Social Security would risk, if not end, its “self-financing” premise.

Moreover, the necessary infusion of general revenues would be large. The trustees currently estimate an OASDI cash deficit of $449 billion in 2034. Over the next 75 years Social Security’s current dedicated revenues fall short of scheduled benefits by about 22 percent. That is the gap that would need to be filled by general revenues.

Social Security is designed to be a self-financing social insurance program, not a general revenue financed support program. Workers and employers pay payroll taxes which are credited to dedicated trust funds. But if the trust funds run dry in 2034, and Congress decides to avoid benefit cuts or tax increases by allowing general revenue transfers, it would break the earned-benefit premise of the program’s original design, increase pressure on the federal budget and undermine public trust in Social Security’s financial integrity.

Charles Blahous, a former Social Security Public Trustee, has warned that general revenue financing of the programs carries the following risks, “First, it would be fiscally irresponsible, essentially adding Social Security’s large financing shortfall to the mushrooming national debt. Second, it would undermine the security and reliability of Social Security benefit payments, as the program would need to compete for financing each year from the general fund, and participants could no longer claim they paid for their benefits. Third, it would be a betrayal of the public trust, as Americans have given no indication that they wish to toss Social Security’s historical design overboard.”

It is worth noting that Blahous, along with his fellow Public Trustee Robert Reischauer, were warning as far back as the 2015 Trustees Report that the situation is not at all the same as it was in 1983 when Congress waited until the last minute to enact reform. They explained in that report:

Throughout much of Social Security’s early history annual income and outgo were kept in reasonably proximate annual balance, such that when the Trust Funds faced a threat of depletion in the early 1980s it was still fully possible, though difficult to be sure, to close the financing gap. After the 1977 and 1983 program amendments, Social Security experienced substantial surpluses of tax income relative to expenditures from the late 1980s through the 2000s. Notwithstanding the fact that the aggregate program has been running annual cash deficits since 2010, these surpluses have accumulated to a substantial positive balance in the hypothetical combined trust funds, one that will peak in 2019 and then decline gradually to depletion in 2034. A critical unintended consequence of large trust fund balances has been that unavoidable corrective actions have been postponed. Continued inaction going forward to the point where the combined trust funds near depletion would—unlike the situation in 1983—likely preclude any plausible opportunity to maintain Social Security’s historical financing structure (emphasis added).

The closer we get to the year when Social Security’s trust funds are depleted, the less feasible it will be to phase-in benefit or tax changes to avoid a solvency crisis and the more likely it will be that Congress chooses to bail out the program with general revenues. This might be seen as the political path of least resistance, but it would end the original premise of Social Security as a self-funded program and dismantle the fiscal backstop provided by the trust funds.

Americans may or may not want this transformation of Social Security to take place, but the decision should not be made by default. We need to confront the stark choices now, deliberate the options and enact a sustainable solution. That would be an appropriate gift to Social Security on its 90th birthday.

Continue Reading