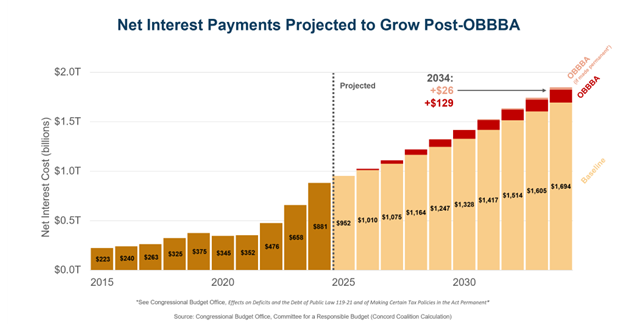

Congress and the President have approved the One Big Beautiful Bill Act (OBBBA), which is projected to increase deficits by $3.4 trillion over the next decade. These unpaid-for tax cuts will worsen our fiscal outlook, drive up the national debt, now at nearly $37 trillion, and add $700 billion in interest payments through 2034, bringing the total deficit increase to $4.1 trillion. Even before this legislation the Congressional Budget Office was projecting that interest costs would rise sharply by 2034, from $952 billion in 2025 to $1.7 trillion. Congress and the President have not chosen solutions, or even inaction, but instead to actively add weight to our already burdensome fiscal situation.

When the federal government borrows funds to finance its expenditures, it sells US treasuries bonds that must be paid back with interest. The interest paid to bondholders is recorded in the budget as an interest expense. The national debt has doubled from 2015 to 2024, but over the same period interest payments have nearly quadrupled from $223 billion in 2015 to $881 billion in 2024. Interest payments have grown faster due to rising interest rates, which have increased in part due to the growing debt. From 2010 to 2020, average interest rates on 10 year treasuries were 2.3% – today they are 4.2%. Because we are carrying so much debt, small changes in rates can have an enormous impact on our national fiscal position. Further according to the Yale Budget Lab, even a modest increase in the deficit can push interest rates higher. These costs will further accelerate in the decade ahead due to the OBBBA debt increase.

Mandatory Debt Service Payments are Taking More Taxpayer Dollars

The federal government must make interest payments on its debts. This is a mandatory federal expenditure, now greater than the amount we spend on defense or Medicare. The more money we spend paying the bills, the less we have to invest in American infrastructure, education, and research & development. Responding to emergencies will also be increasingly difficult with less budgetary flexibility. We must acknowledge the true costs of stacking up our bills faster than we can pay them down.

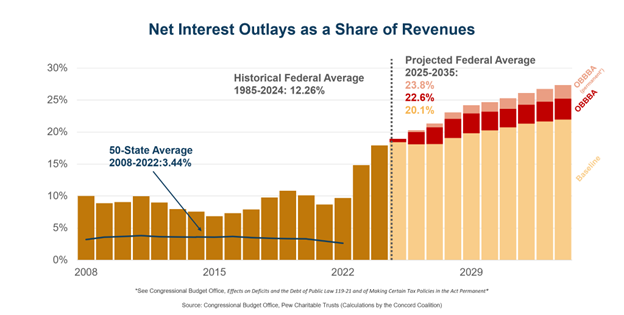

A common metric for measuring the affordability of debt is interest payments as a share of revenue. In other words, how much of the revenue the government is collecting must be used to pay interest on the debt. In Moody’s downgrade of the United States credit rating, they cited a sharply rising debt service to revenue ratio over the next decade. Bond rating agencies will often use this same metric to assess U.S. states’ creditworthiness and capability to borrow. States on average use 3.4% of their revenue to pay debt service costs. Some states have statutory or constitutional rules that limit or place a cap on the debt service to revenue ratio. It’s common for these limits to fall between 5% to 10%.

Meanwhile over the next 10 years, federal debt service payments will be, on average, 22.6% of revenues collected, reaching more than 25% in 2034. That means one out of every four taxpayer dollars will be paying interest on the debt. If lawmakers extend temporary OBBBA tax provisions, debt service would exceed 27% of revenues in 2034.

The danger here is that we are in an increasingly precarious economic position where growing interest payments squeeze out our ability to invest in other domestic priorities and drive up interest rates crowding out private investment. This effect can create a long term drag on our economy, if not precipitate an outright fiscal crisis with severe economic consequences (likely high inflation and high interest rates). Congress and the President should seriously consider options to slow the growth of our debt and bring the federal budget under control.

Continue Reading