As Medicare celebrated its 60th anniversary last week, much of the discussion about its financial future centered on a single, ominous metric: the depletion date of the Hospital Insurance trust fund (HI). Medicare’s Trustees say this will happen in 2033, just eight years away. That date serves as a clarion call for action because depletion of the HI trust fund would trigger across-the-board provider cuts, jeopardizing access to healthcare for millions of seniors. But while the impending HI shortfall deserves prompt attention, a singular focus on that problem obscures the larger fiscal threat posed by Medicare’s Supplementary Medical Insurance trust fund (SMI).

Medicare has multiple components, and they are funded in very different ways. The HI trust fund (Medicare Part A) pays for inpatient hospital care, skilled nursing facilities, hospice, and some home health care. It is financed primarily by a 2.9% payroll tax and has a modest reserve of about $200 billion. If the trust fund is depleted (the reserve gets spent to $0), payments to providers would have to be cut to match current income, which would fall short of funding all scheduled benefits. The Medicare Trustees estimated in their 2025 report that provider payments would need to be cut by 11 percent upon trust fund insolvency in 2033.

The SMI trust fund, (Medicare Parts B and D) covers physician services, outpatient care and prescription drugs. It is funded through a combination of beneficiary premiums and general revenue transfers from the Treasury. Unlike the HI trust fund, the SMI trust fund receives no funding from the payroll tax. The premiums paid by beneficiaries who enroll in Parts B and D are set each year to cover just 25 percent of expected costs, meaning that the vast majority of the program (75 percent) is funded by general revenue transfers.

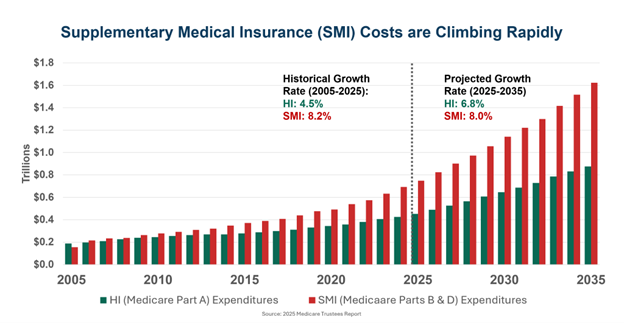

Throughout the first decades of Medicare’s existence, the HI trust fund paid the largest share of the program’s total expenses and the payroll tax was the dominant source of income. That has changed substantially because of the growth of Part B and the creation of Part D (prescription drugs) in 2004. SMI now accounts for the majority of Medicare spending.

According to the Medicare Trustees, HI spending was $423 billion in 2024 compared to SMI spending of $700 billion. This trend is expected to continue. By 2035, the Trustees project that HI and SMI spending will both more than double but SMI is far more expensive.

Given these growth projections, the structural difference in the respective sources of income for HI and SMI has major implications for the federal budget. The HI trust fund is constrained by its dedicated revenue and can be depleted. This provides a check on expenses because it forces Congress to at least do something before sudden deep cuts automatically take effect.

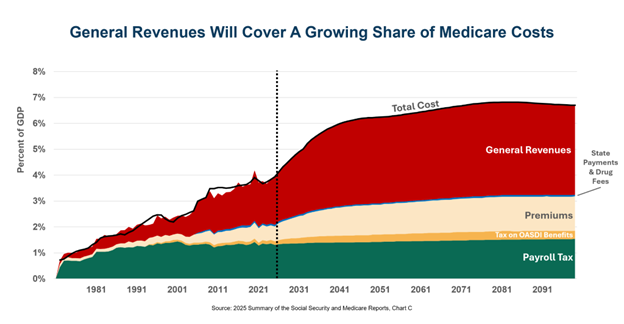

In contrast, the SMI trust fund can never be depleted because it has an open pipeline to the U.S. Treasury for 75 percent of its expenses regardless of the cost. There is no blinking red light warning of trust fund insolvency and no “crisis point” of payment cuts as there is with HI—only steadily rising general revenue transfers that pose a growing burden on the federal budget. As a result, SMI is a far greater contributor than HI to Medicare’s long-term cost growth and an even bigger challenge to federal budget sustainability.

Ironically, because SMI is never at risk of “running out of money,” it doesn’t attract the same level of attention or urgency as the smaller and better funded HI trust fund. Every year, the federal government simply adjusts the required general revenue contribution upward to cover SMI’s growing costs. The budgetary consequences are automatic and hidden in the broader federal deficit.

This creates an odd fiscal illusion. The HI trust fund is treated as an impending crisis because insolvency triggers legal consequences, but the SMI trust fund is seen as stable—even though its open-ended structure creates a larger and growing fiscal burden.

Medicare’s Trustees have explicitly warned about the unconstrained growth of SMI and its impact on the federal budget. In this year’s report, they summed it up as follows:

The Trustees expect growth in SMI Part B and Part D premiums and transfers from the general fund of the Treasury to continue to outpace GDP growth and HI payroll tax growth in the future. This phenomenon occurs primarily because SMI revenue increases at the same rate as expenditures, whereas HI revenue does not. Accordingly, as the HI revenue sources become increasingly inadequate to cover HI costs, SMI revenues will represent a growing share of total Medicare revenues. Government contributions are projected to gradually increase from 45 percent of Medicare financing in 2024 to about 50 percent in 2036, stabilizing thereafter. Growth in these contributions as a share of GDP adds significantly to the Federal budget pressures.

A similar warning has been issued by the Medicare Payment Advisory Commission (MedPAC), an independent congressional agency that advises Congress on Medicare issues. The July 2025 MedPac Data Book states:

General tax revenue transfers currently pay for nearly half of Medicare spending and are expected to continue to do so in future decades…. As increasing amounts of general tax revenues have been devoted to Medicare, less tax revenue has been available for other priorities such as deficit reduction or investments that could grow the economic output of the country (e.g., federal investments in research and development, education, and transportation).

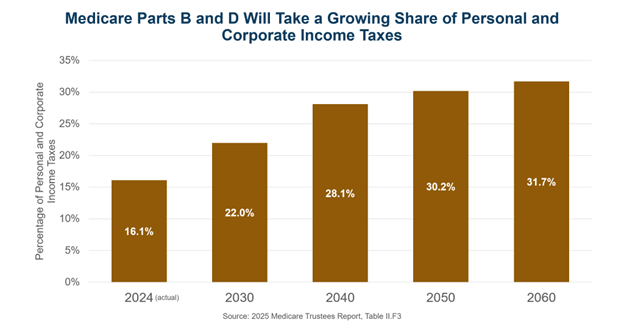

To put SMI’s general revenue transfers into context, the Medicare Trustees produce a table showing those transfers as a share of gross domestic product (GDP) compared with total personal and corporate federal income taxes (assuming that those taxes remain at their historical average level of the last 50 years). It shows that SMI transfers could, by themselves, consume nearly one-third of federal income taxes within 25 to 30 years.

There is still time—and flexibility—to address this challenge thoughtfully as suggested by the Trustees, who said in their 2025 report, “Current-law projections indicate that Medicare still faces a substantial financial shortfall that needs to be addressed with further legislation. Such legislation should be enacted sooner rather than later to minimize the impact on beneficiaries, providers, and taxpayers”

The first step is to recognize that Medicare’s biggest fiscal problem is not the one that’s most visible. It’s the one that’s hiding in plain sight.

Continue Reading