Concord Action welcomes a variety of viewpoints on issues related to the long-term fiscal health of the nation. The following is a guest essay written by Aaron Till, senior policy analyst with the Bipartisan Policy Center.

The U.S. publicly held national debt is on track to reach 120% of gross domestic product (GDP) by 2035. Growing debt puts upward pressure on interest rates, crowding out private investment and driving up the cost of living. Congress must act with urgency to achieve fiscal sustainability, and it needs a plan to get there.

The current budget process is not conducive to progress on deficit reduction. As it stands, the process defaults towards unchecked spending and unpaid-for tax cuts. To achieve long-term stability, Congress must implement comprehensive, structural changes to the federal budget process.

Lessons from Past Budget Process Reforms

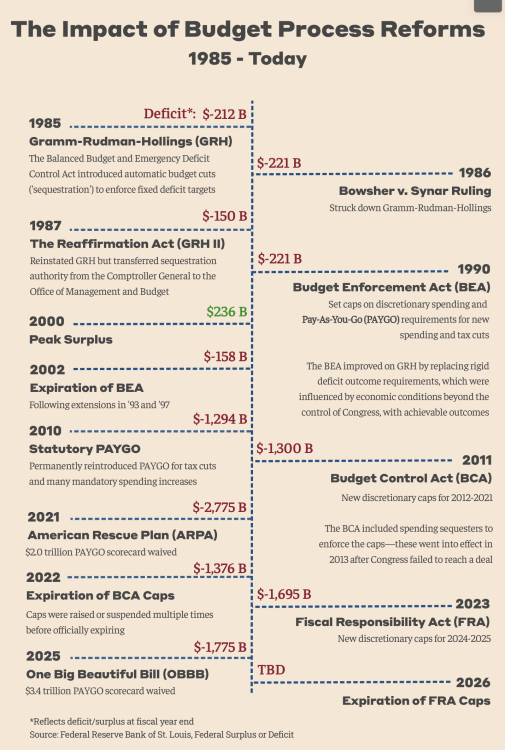

Through the years, Congress has tried different budget process reforms with mixed results. It has set budgetary targets and caps, created requirements to offset the costs of new spending or tax cuts, and imposed automatic backstops for enforcement.

One successful attempt, the Budget Enforcement Act (BEA) of 1990, set limits on discretionary spending (caps) and introduced Pay-As-You-Go requirements for mandatory spending (PAYGO) and revenue changes. PAYGO instructs Congress to pay (i.e., find offsets) for any new increases in mandatory spending or tax cuts—failure to do so leads to across-the-board spending cuts (sequesters) to all non-exempt programs. The BEA helped achieve a balanced budget between 1998 and 2001.

Since then, however, a variety of exemptions have limited the effectiveness of the BEA, contributing to today’s mounting debt burden. For instance, certain appropriations are regularly designated as emergency spending, meaning they aren’t counted towards budget caps. Furthermore, Congress has a history of allowing caps and PAYGO requirements to expire for several years before implementing new versions. Even when the provisions are in effect, lawmakers have at times passed special legislation to waive the consequences. The following timeline shows an abridged history of various reforms to the federal budget process.

Most recently, discretionary spending caps were included as part of the Fiscal Responsibility Act (FRA) of 2023. These caps expired prior to fiscal year 2026, however, meaning that the only remaining measure of fiscal discipline is the permanent PAYGO provisions (statutory PAYGO) enacted in 2010.

Most recently, discretionary spending caps were included as part of the Fiscal Responsibility Act (FRA) of 2023. These caps expired prior to fiscal year 2026, however, meaning that the only remaining measure of fiscal discipline is the permanent PAYGO provisions (statutory PAYGO) enacted in 2010.

Unfortunately, PAYGO is frequently ignored by Congress regardless of the political party in control. Most recently, Congress waived $3.4 trillion in PAYGO “debt” from the One Big Beautiful Bill (OBBB). The Congressional Budget Office estimated that PAYGO sequestration, if enforced with OBBB, would have exceeded the entirety of the funding available in programs subject to sequestration.

As a first step towards fiscal responsibility, Congress should stop digging the budget hole deeper and abide by existing PAYGO restrictions moving forward rather than trying to circumvent them. In the current fiscal environment, however, doing so would still be insufficient to reverse runaway deficits.

To meet the moment, Congress should explore new options for enforcement regimes that mandate actual deficit reduction rather than just offsets for new spending or tax cuts. Lessons can be drawn from past proposals, such as BPC’s SAVEGO or the Committee for a Responsible Federal Budget’s Super PAYGO. Complementary budget process reforms could be enacted simultaneously, such as restoring the Conrad Rule, which prohibits increasing the deficit through reconciliation. BPC Action has supported several legislative actions to improve our fiscal state, including the Fiscal Commission Act and the Responsible Budgeting Act.

Potential Components of a New Enforcement Mechanism

Congress should ask itself key questions when crafting a new enforcement mechanism to maximize its potential for success:

- What are meaningful and achievable budgetary targets to reduce the debt? One shortcoming of the Gramm-Rudman-Hollings Act of 1985 was that it included fixed deficit targets that were influenced by economic factors beyond the control of Congress. Under fixed deficit models, economic downturns necessitate fiscal contractions, potentially extending the recession’s duration, while economic booms encourage spending bonanzas that are hard to scale back.

- For example, strong economic growth and tax revenue in the late 1980s allowed Congress to continually increase spending under GRH, only to walk into a deficit spike in the 1990 recession.

- Rather than a fixed deficit level, targets could be pegged to a cumulative reduction in debt or an average deficit reduction over a multi-year period, incentivizing Congress to save during economic expansions. To minimize economic disruption, Congress could aim to achieve some interim target, such as lowering the deficit to 3% of GDP by a specific year.

- How should targets be achieved across the entire budget? Topline targets are just the start. The real challenge for Congress is to weigh the tradeoffs required to achieve them. Past reforms set discretionary spending caps across different categories, such as defense and non-defense (FRA and the Budget Control Act of 2011) and defense, domestic, and international (BEA). Some critics have pointed out that existing sequesters disproportionately impact discretionary funds, leaving most entitlement spending untouched. Given the enormity of deficits today, and the fact that they are largely driven by automatic mandatory spending and insufficient revenues, lawmakers will need to negotiate how to allocate saving targets across the entire budget. BPC’s previous SAVEGO proposal, for example, recommended budgets for discretionary spending programs, major health programs, and other mandatory spending and tax expenditures.

- How should Congress enforce its targets? The key element in any fiscal responsibility framework is a backstop if Congress falls short of its savings targets. Effective enforcement mechanisms must be compelling for both parties, but excessively painful consequences can backfire if they lead to congressional overrides. Automatic sequestration of discretionary and some mandatory spending has been a common mechanism underlying past budget reforms, but enforcement regimes need not be limited to spending cuts. Creative and more balanced approaches could consider including surtaxes or other revenue raisers like curbing tax expenditures—measures that might increase bipartisan buy-in on achieving fiscal targets.

Taming the federal debt will be a multiyear—perhaps multidecade—process that spans multiple Congresses. Achieving this goal could be assisted by Congress adhering to a plan: specifically, a procedural blueprint to help future legislators maintain a path of fiscal responsibility.

While political leadership and bipartisan buy-in to reduce current spending and increase revenues are the most important steps in addressing our debt crisis, we cannot achieve long-term stability without structural changes. We need a budget process that encourages savings.

Continue Reading