As homebuyers across the country grapple with persistently high mortgage rates, many are asking: Why is borrowing to buy a home getting so expensive? While inflation and Federal Reserve policy play a role, there’s another powerful—and often overlooked—factor at work: the growing federal debt.

The Debt-Interest Rate Connection

When the federal government runs large deficits, it must borrow money to cover the gap—primarily by issuing Treasury securities. As the supply of government debt increases, the government competes with households and businesses for available capital in financial markets. This competition can push interest rates higher, especially when investors demand higher yields to absorb the growing supply of debt.

At the same time, if the government is borrowing more and more, lenders (investors) may demand higher interest rates to compensate for inflation or future higher tax burdens to pay down the debt. Inflation is a concern because debt bought today is worth less at maturity if inflation increases over that period. To compensate, they demand higher returns. That means higher interest rates—not just for the government, but for everyone.

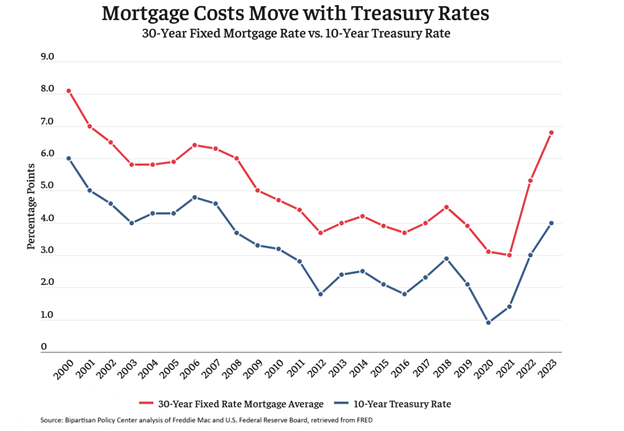

Why Mortgage Rates Follow Treasury Yields

One of the most immediate ways this impacts everyday Americans is through mortgage rates. Although many factors influence these rates—like housing supply and demand—the interest rate on a typical 30-year fixed mortgage often rises and falls alongside the yield on the 10-year U.S. Treasury note. Why? Because mortgage-backed securities (MBS)—which are bundles of home loans sold to investors—are priced by the market in relation to Treasury yields. When Treasury yields go up, investors expect higher returns on MBS as well. That demand for higher returns leads to higher mortgage rates for borrowers.

So when federal borrowing drives up Treasury yields, it indirectly drives up the cost of buying a home.

What the Research Shows

Economists have long debated how much federal debt affects interest rates. But a growing body of research is converging on a rule of thumb: for every 1 percentage point increase in the debt-to-GDP ratio, long-term interest rates rise by about 4 basis points (0.04 percentage points).

That may sound small, but it adds up. If debt rises by 20 percentage points of GDP—as it did between 2019 and 2025, from 79% to 99% of GDP—that could mean an increase of 0.8 percentage points in long-term interest rates. On a $400,000 mortgage, that’s roughly $2,400 more per year in payments. Debt is projected to increase another 20 percentage points of GDP over the next ten years further reducing housing affordability.

Why It Matters

Higher mortgage rates don’t just affect homebuyers—they ripple through the entire economy. They reduce home affordability, slow construction, and dampen consumer spending. And for younger Americans trying to build wealth through homeownership, the consequences are especially acute.

The Bottom Line

Federal borrowing isn’t just a Washington problem—it’s a kitchen table issue. As the national debt climbs past $38 trillion, the cost isn’t just abstract. It’s showing up in your mortgage quote, your rent, and your family’s financial future.

If we want to make housing more affordable and interest rates more stable, we need to get serious about fiscal responsibility. That means addressing the drivers of long-term debt—not just to balance the books, but to protect economic opportunities for the next generation.

Continue Reading